Compliance Alert: Rate Reset Notices for Adjustable-Rate Mortgages Using LIBOR as an Index

The London Interbank Offered Rate (LIBOR) ended after December 31, 2021, for the one-week and two-month U.S. dollar (USD) tenors and will end after June 30, 2023, for the remaining overnight, one-month, three-month, six-month, and 12-month USD tenors. To facilitate the transition from LIBOR for consumer credit products, the Consumer Financial Protection Bureau (Bureau) published a final rule1 in December 2021 establishing the compliance requirements for 1) replacement indexes for variable-rate products, 2)change-in-terms notices, and 3) reevaluations of credit card rate increases. Consumer Compliance Outlook reviewed these requirements in Issue 1 2022.2 In this related compliance alert, we address the effect of LIBOR’s sunset on the required rate reset notices sent to borrowers with adjustable-rate mortgages (ARMs) in advance of the reset.

NOTICE OF CHANGE TO PAYMENT WHEN RATE ADJUSTS: §1026.20(c)

An ARM, which is defined as a closed-end consumer credit transaction secured by the consumer’s principal dwelling in which the annual percentage rate may increase after consummation, has specific disclosure requirements under Regulation Z.3 With some exceptions,4 when a rate is scheduled to reset under the loan agreement that will cause the payment to change, the borrower must be notified in advance and provided detailed information about the change.

Under 12 C.F.R. §1026.20(c)(2), the required disclosures in a reset notice include the index used to calculate the interest rate adjustments and a source of information about the index or formula. Accordingly, the reset notices for ARMs using LIBOR as an index will have to be updated to reflect the replacement index and source of information about it, as discussed next.

Disclosure Requirements

Section 1026.20 specifies the rate-change disclosure requirements for the initial reset and subsequent resets in 12 C.F.R. §1026(d) and (c), respectively.

Timing

Initial Reset

The first reset notice must be sent between 210 and 240 days before the first payment — at the adjusted level — is due; see 12 C.F.R. §1026.20(d).

Subsequent Resets

- If the rate resets less frequently than every 60 days, the notice must be provided between 60 and 120 days before the payment is due at the adjusted level; see 12 C.F.R. §1026.20(c)(2).

- If the rate resets every 60 days or more frequently, the notice must be provided between 25 and 120 days before the payment is due at the adjusted level; see 12 C.F.R. §1026.20(c)(2).

Format and Model Forms

Initial Reset Notice

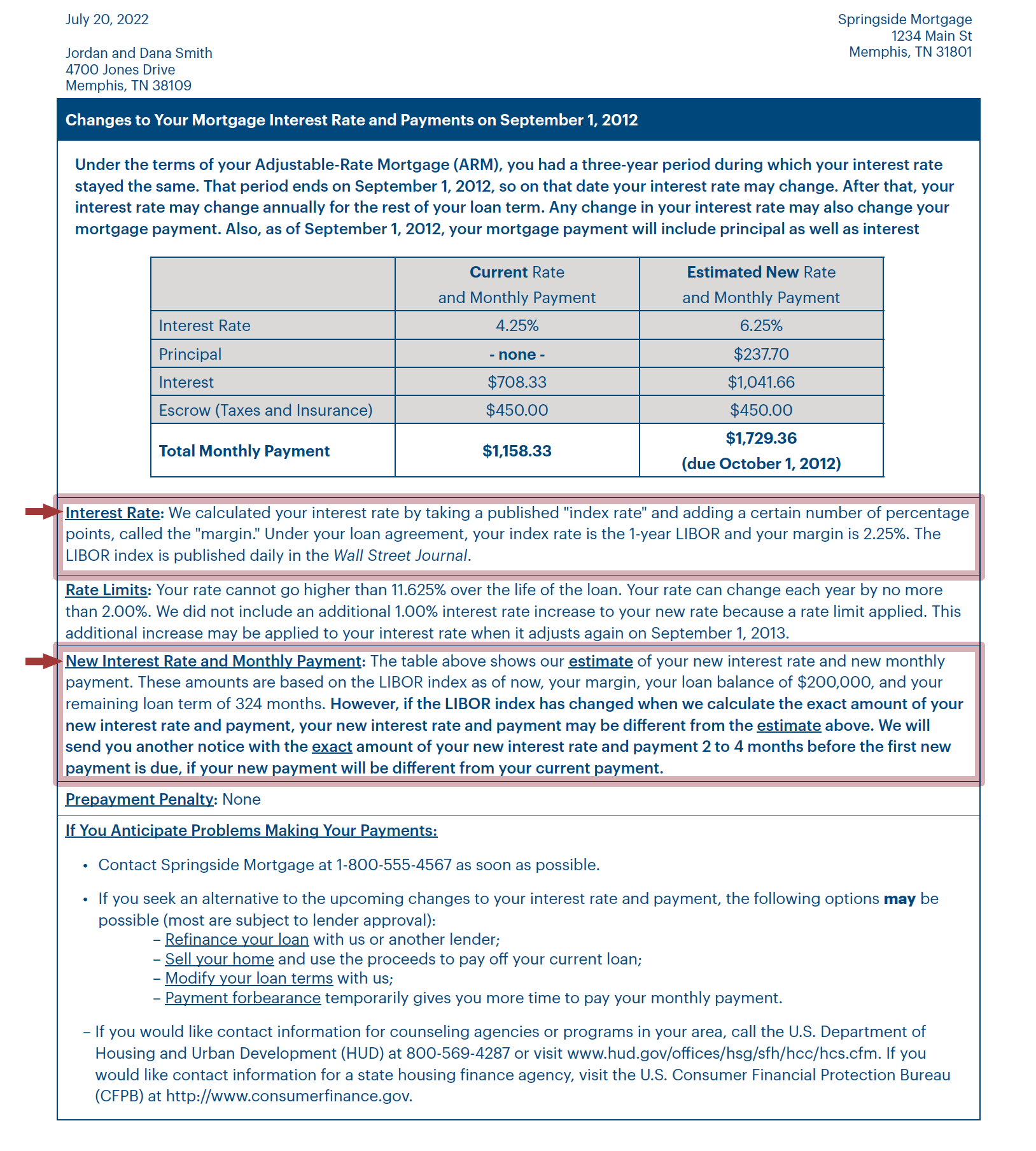

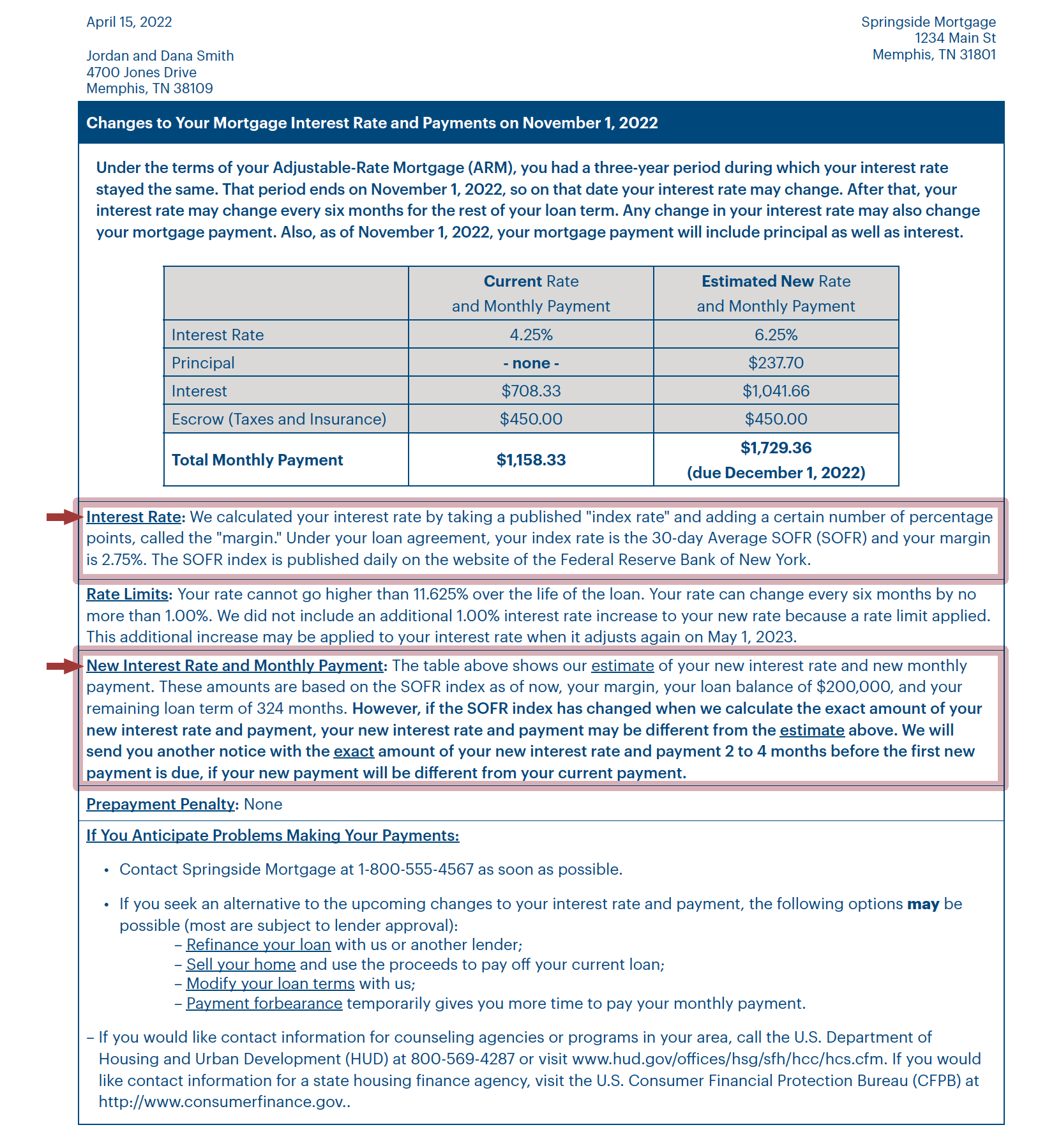

The rate change information for the initial reset must be disclosed in a tabular format substantially similar to the model form in H-4(D)(3) in Appendix H of Regulation Z using the same order, headings, and format.5 To facilitate compliance, two sample forms are provided in sample form H-4(D)(4): one for LIBOR that can be used until September 30, 2023, and another that can be used on or after April 1, 2022, which uses the Secured Overnight Financing Rate as the illustrative replacement index. We reproduce these two sample forms as Figures 1 and 2 at the end of this alert.

{kind=link}

{kind=link}

{kind=link}

Subsequent Rate Reset Notices

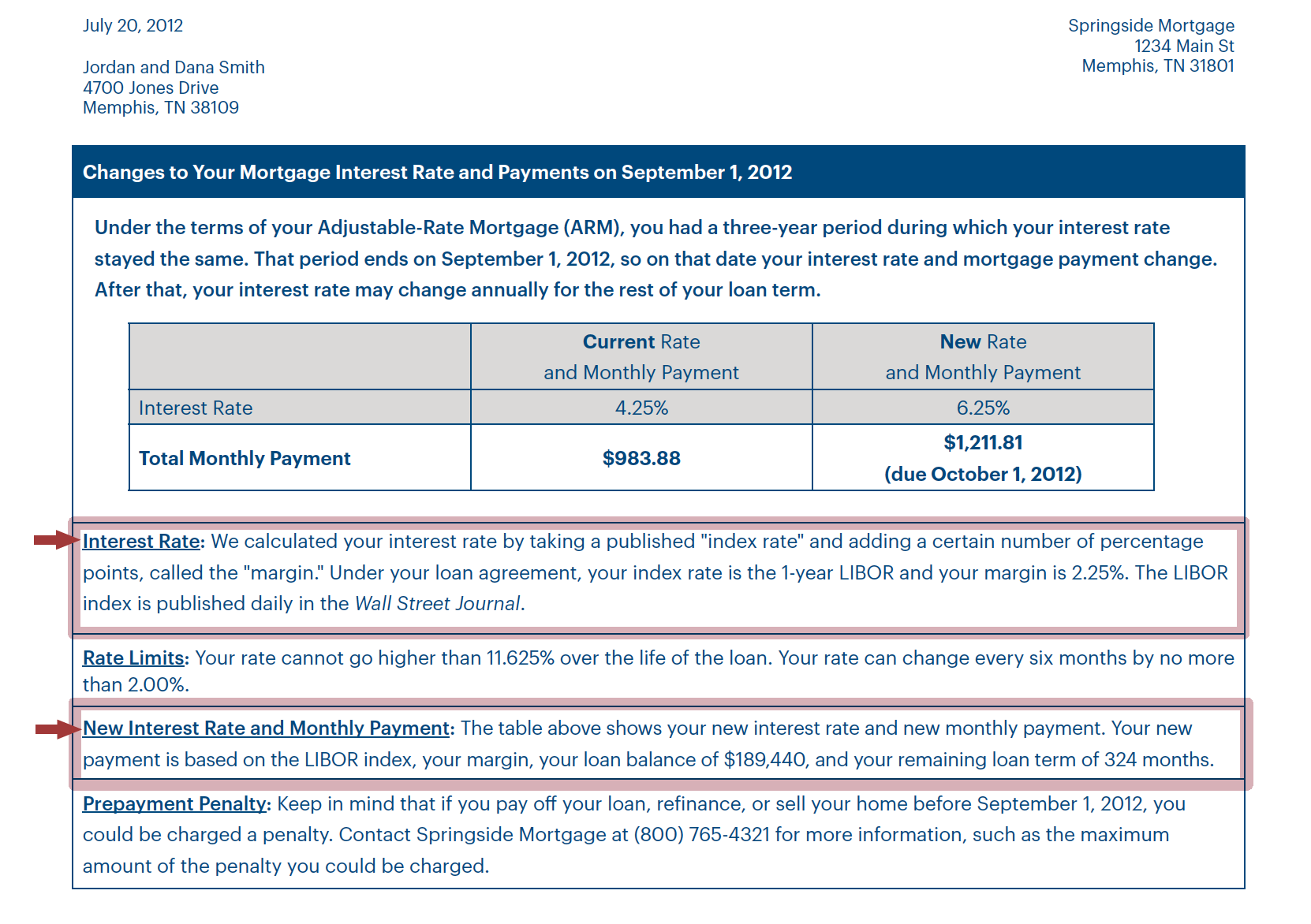

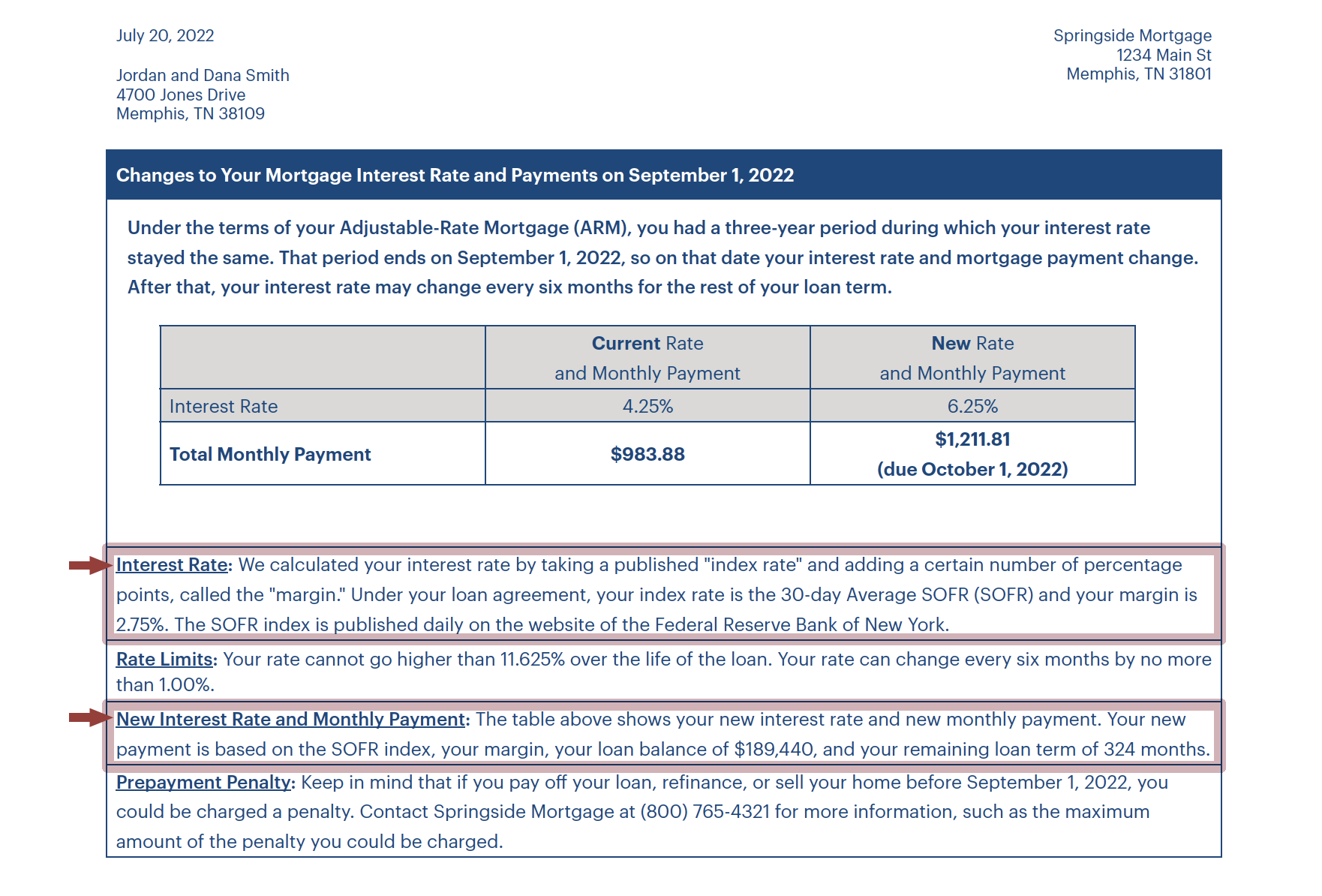

Subsequent reset notices must be provided in the form of a table and in the same order as — and with headings and format substantially similar to — Model Form H-4(D)(1) in Appendix H.6 Two sample forms (one for LIBOR, which may be used until September 30, 2023, and one for the replacement index which can be used on or after April 1, 2022) are provided in H-4(D)(2). We reproduce these two sample forms as Figures 3 and 4 at the end of this alert.

{kind=link}

As LIBOR’s final sunset date approaches, creditors for ARMs using LIBOR as an index must update their rate reset notices in their systems to reflect the replacement index. Additional information is available in the Bureau’s LIBOR transition FAQs.

Figure 1: Legacy LIBOR Initial Rate Reset Form7

Can Only Be Used Through September 30, 2023

Figure 2: Revised Form for Initial Rate Reset8

Can Be Used on or After April 1, 2022

Figure 3: Legacy Form for Subsequent Rate Resets9

Can Only Be Used Through September 30, 2023

Figure 4: Revised Form for Subsequent Rate Resets10

Can Be Used on or After April 1, 2022

ENDNOTES

1 See 86 Federal Register 69716 (December 8, 2021).

2 Kenneth J. Benton, “The Bureau’s Final Rule Under Regulation Z to Address LIBOR’s Sunset,” Consumer Compliance Outlook (Issue 1 2022).

3 See 12 C.F.R. §1026.20(c)(1).

4 See 12 C.F.R. §1026.20(c)(1)(ii).

5 See 12 C.F.R. §1026.20(d)(3). But creditors and servicers are permitted to modify the disclosures to accommodate particular consumer circumstances or transactions not addressed by the forms. For example, in the case of a consumer bankruptcy or under certain state laws, the creditor, assignee, or servicer may modify the forms to remove language regarding personal liability. See Comment 20(d)(3)(i)-1.

6 See 12 C.F.R. §1026.20(c)(3).

7 See Sample Form H-4(D)(4).

8 See Sample Form H-4(D)(4).

9 See Sample Form H-4(D)(2).

{kind=link}

10 See Sample Form H-4(D)(2).