An Overview of Community Development Financial Institutions

The economic impacts of the COVID-19 pandemic and the subsequent recovery response underscore the importance of Community Development Financial Institutions (CDFIs) in responding to the financial needs of historically underserved consumers and borrowers in times of crisis.1 In a recent conversation, Calvin Holmes, president of the Chicago Community Loan Fund, a Chicago-based CDFI, described CDFIs as “financial first responders, who run into the face of danger to triage and treat those who need it most.” To build on the allegory further, this article identifies the “financial triage centers,” probes how they operate, examines several new tools in CDFIs’ “first aid kits,” and diagnoses challenges CDFIs face in ensuring the “capillaries” of our nation’s financial system channel credit and capital to low- and moderate-income (LMI) communities and communities of color.2

What Is a CDFI?

At the simplest level, a CDFI is a private financial institution whose mission is to provide financial products and services, along with training and technical assistance, to underserved communities, including LMI consumers, communities of color, women, or minority groups who can experience challenges accessing credit. CDFIs deliver financial community assets in disinvested places, whether they are rural, urban, suburban, or otherwise. CDFIs exist to help grow local economies, provide affordable housing, and support small minority-owned businesses. CDFIs offer a creative solution to counterbalance harmful practices such as redlining, a historical practice that continues to have implications for the racial wealth divide in the U.S.3 The U.S. Department of the Treasury administers the CDFI Fund, to which certified CDFIs can apply for certain types of financial benefits.4

Common uses of CDFI loans include financing affordable housing developments, commercial real estate, small businesses, community centers, nonprofit and religious institutions that provide community benefits, and health-care centers. As of September 2021, 1,390 CDFIs were certified, and all 50 states and several U.S. territories have at least one certified CDFI.5

The 1994 Riegle Community Development and Regulatory Improvement Act6 established the Community Development Financial Institutions Fund. This law defined the requirements for organizations to attain CDFI status and increased access to federal resources through the congressional appropriations process to support organizations that fill gaps in financing for economically disadvantaged communities. Subsequent congressional legislation such as the 2009 American Recovery and Reinvestment Act, the 2010 JOBS Act, and the 2021 American Rescue Plan Act established additional conduits through which the CDFI Fund can provide federal funding to reach deeper into communities where access to credit and capital remain a barrier to economic growth.

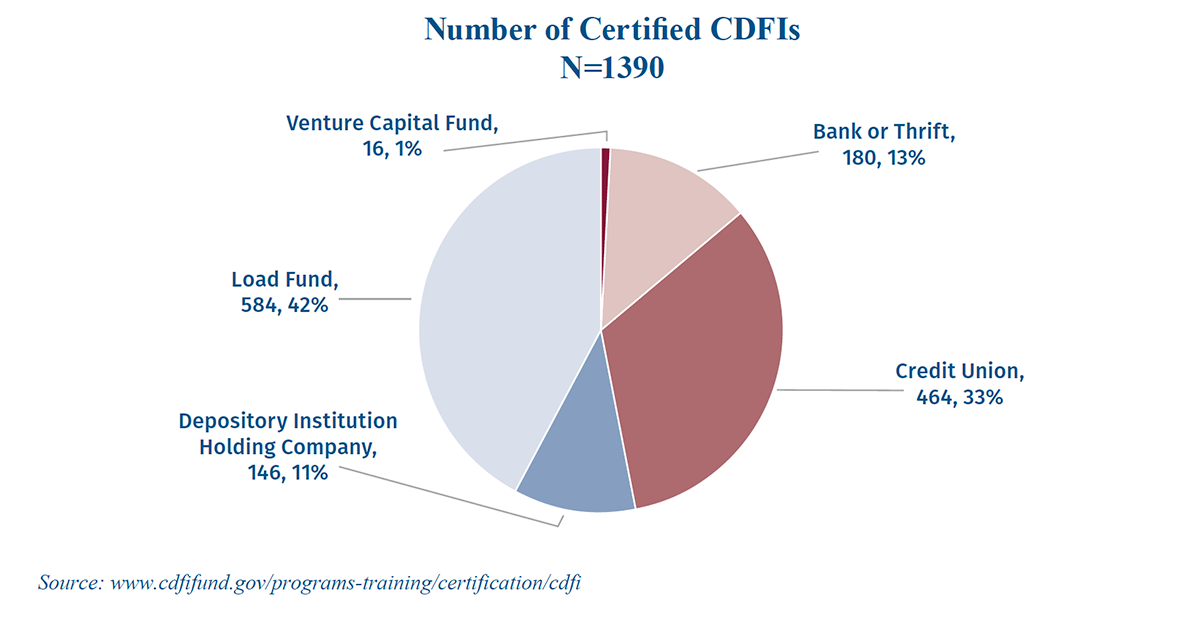

More broadly, certified CDFIs can be separated into two groups: 1) depository CDFIs that consist of banks, thrifts, depository institutions, and credit unions, including Minority Depository Institutions; and 2) nondepository CDFIs, many of which are not-for-profit loan funds, and venture capital funds (Figure 1). In terms of total portfolio amounts, in 2020, depository CDFIs held 83.6 percent of the CDFI industry’s loan dollar value and composed about 50 percent of the industry, while loan funds largely comprised the other half of the industry.7 The Treasury Department annually reviews certified CDFIs to ensure their business model still meets the Congressionally mandated CDFI requirements.8

Figure 1: CDFIs by the Numbers

Source: CDFI Fund Certification Data, CDFI_Cert_List_02_14_2022_Final.xlsx (live.com) (02/14/2022)

How CDFIs Operate

Business Model

At its core, the business model of a CDFI is to lend money, while having a socioeconomic return for an identified community with location-based or identity-related characteristics.9 CDFIs must obtain capital to pay for the loans they disburse to clients, along with the salaries and operations that help underwrite and service loans, as well as provide technical assistance to clients. The specialization of CDFIs lies in their ability to acquire and blend various forms of capital so they can make loans that others will not or cannot.

One key source of capital for certified CDFIs is the CDFI Fund, which considers applications for grants, loans, and, in some cases, equity from the CDFI Fund and other federal programs, many of which use CDFI certification as a preliminary requirement to access funds.10 The need for alternative access to credit and capital in LMI and minority communities exceeds taxpayer funding provided through the congressional appropriations process. As a result, CDFIs use these funds to leverage private capital. For example, the interest rates and fees nonprofit loan fund CDFIs charge are designed to be affordable for economically distressed clients, but are typically not enough to cover the entire cost of lending operations.11 CDFIs must therefore rely on other earned income, grant donations, fundraising, equity investments, debt instruments, and — in the case of CDFI banks and credit unions — deposits to support their business models.

In addition to the aforementioned CDFI certification provided by the Treasury Department and its affiliated funding programs for certified CDFIs, numerous federal agencies and others administer programs that provide capital, technical support, or research for CDFIs, including the Board of Governors of the Federal Reserve System, Small Business Administration (SBA), Department of Housing and Urban Development (HUD), FDIC, Office of the Comptroller of the Currency (OCC), National Credit Union Administration (NCUA), Department of Agriculture, and private entities, including banks through the CRA. Some corporations and foundations also have resources available for CDFIs.12

CDFIs’ Role in Financial Inclusion

CDFIs, CRA-motivated banks, philanthropies, and private investors help comprise what CDFI practitioners call the “community development finance ecosystem.”13 Entities, community members, and other nonprofits and small businesses operate symbiotically within this community development finance ecosystem. CDFI loans and investments support catalytic community assets that help to grow local economies, revitalize disinvested places, and uplift downtrodden communities with legacies of racial exclusion.

These typically hyper-local, mission-driven financial institutions play a key role in improving financial and economic inclusion, especially in challenging times. While recent data on the industry’s performance as a whole are limited because of the nonprofit status of half the industry and a lag in CDFI Fund reporting requirements, we know from the Great Recession that CDFIs concentrate their lending activity in census tracts with signs of distress such as high poverty or unemployment rates, even more so than conventional lenders.14, 15 Further, based on call reports and other public information about subsets of the CDFI industry, we know that many, if not most, CDFIs have historically maintained charge-off rates comparable to traditional depository institutions, all while serving clients that other lenders deem too risky.16

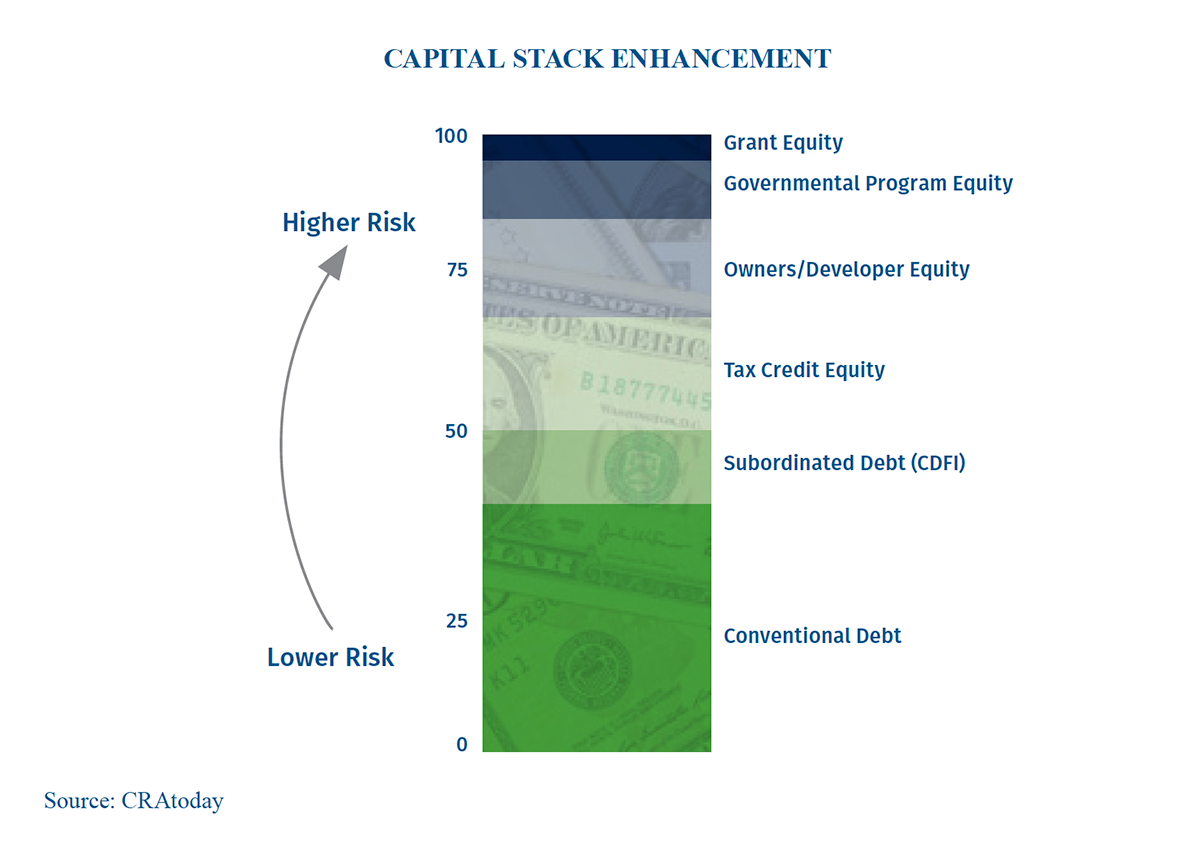

By creatively blending federal, private, philanthropic, and state and local funding, community-based lenders develop a diversified stack of capital to cushion more risk-averse funders from losses, while stretching and leveraging dollars further than one source of capital alone would have provided. This stitching together of different kinds of capital to fund community investments is where CDFIs adroitly blend different funding sources based on investors’ risk tolerance to create viable financial transactions (Figure 2).17

Figure 2: Blending Funding Sources Based on Risk Tolerance

All of these resources together help support a healthy ecosystem of financial services available to individuals and households along the financial inclusion spectrum. As the COVID-19 pandemic reemphasized, researchers continually demonstrate that low-and moderate-income communities, communities of color, and women have a harder time accessing capital from traditional financial institutions overall.18

A Variety of Instruments

Within the realm of CDFIs, entities can obtain designations, apart from their depository or nondepository status or for-profit or nonprofit status, that help to attract specific types of funding that can be used to develop unique capital stacks for diverse and distinct financing transactions.

For example, one CDFI segment focuses exclusively on supporting Native American communities across the country. These Native American CDFIs provide essential capital in some of the most historically disinvested parts of our nation with the highest unemployment and poverty rates and the greatest need for alternative sources of capital.19

Because Minority Depository Institutions (MDIs) are generally chartered to lend in and provide services to underserved communities, they typically satisfy the standards of a certified CDFI. An MDI is defined in the Financial Institutions Reform, Recovery and Enforcement Act of 1989 as a “depository institution where 51 percent or more of the stock is owned by one or more ‘socially and economically disadvantaged individuals.’”20 Not all MDIs are CDFIs, however, and only those MDIs that apply for CDFI certification from the Treasury Department can tout their status as both types of entities. Currently, there are 144 MDIs, 32 of which are also CDFIs.21

CDFI Companions

Several of the CDFI Fund’s programs exist to support entities that are not necessarily certified CDFIs but have similar missions and purposes to certified CDFIs. For example, the Capital Magnet Fund provides “competitively awarded grants to CDFIs and qualified non-profit housing organizations” to finance affordable housing activities, related economic development activities, and community service facilities.22

Another program that certified CDFIs and CDFI-like entities can potentially access is the New Markets Tax Credit Program (NMTC). Through the NMTC, individual and corporate investors can receive a tax credit against their federal income tax in exchange for making equity investments in specialized financial intermediaries called Community Development Entities or CDEs. CDEs must also apply for that designation, have a primary mission of serving low-income communities, and maintain accountability to the residents of their targeted low-income communities.

Bank Enterprise Awardees are FDIC-insured depository institutions that have been awarded by the CDFI Fund for “increasing their investments and support of CDFIs and advancing their community development financing and service activities in the most economically distressed communities.”23 The program leverages federal investments with private funds, multiplying the funding that can be used to support affordable housing, improve access to finance, and grow local, distressed economies.24

Another CDFI program that encourages CDFI banks, banks, and nondepository CDFIs to collaborate is the CDFI Fund’s Small Dollar Loan Program (SDLP), which launched its inaugural round in September 2021.25 The SDLP’s purpose is to expand consumer access to financial institutions by providing alternatives to high-cost, small-dollar lending, such as payday loans and check cashers, which nearly a quarter of American households use in lieu of traditional bank accounts.26 By providing funds to support Loan Loss Reserves and Technical Assistance, certified CDFIs are encouraged to establish and maintain small-dollar loan programs that provide term loans of no more than $2,500. While these loan amounts may seem small individually, in aggregate, U.S. consumers borrow nearly $90 billion every year in short-term, small-dollar loans that typically range from $300 to $5,000.27 Given the market size, and the increased demand for funding because of the COVID-19 pandemic, the SDLP is an important source of institutional capacity building to provide small-dollar loans.

“Newer” CDFI Resources

In addition to the CDFI-focused financial resources and programs discussed previously, the COVID-19 pandemic, the racial injustices it exposed, and subsequent responses catalyzed various new types of capital or support for certified CDFIs. Each provides a specific tool to help CDFIs lend to their designated target markets — some delivering liquidity so that CDFIs free up their balance sheets and continue to lend, some providing loan loss reserves so that CDFIs can shore up their portfolios from anticipated loan losses, and some providing direct lending capital or operating support, among other uses.

Emergency Capital Investment Program (ECIP)

One of the newer federal programs available to CDFIs and MDIs is the Treasury’s Emergency Capital Investment Program (ECIP), which Congress created in response to the pandemic in the Consolidated Appropriations Act of 2021 to augment CDFIs’ efforts to support small businesses and consumers in their communities. The program provides capital to certified CDFIs “to provide loans, grants, and forbearance for small businesses, minority-owned businesses, and consumers, especially in low-income and underserved communities, that may be disproportionately impacted by the economic effects of the COVID-19 pandemic.” The Treasury Department recently awarded $9 billion in capital directly to 160 CDFI banks and 59 MDIs.28 The banking agencies have helped implement the ECIP. For example, the Board, OCC, and FDIC recently released an accompanying interim final rule to provide the regulatory capital treatment for instruments issued under the program. Depending on its implementation, ECIP has the potential to provide an important source of previously unavailable Tier One capital for CDFI banks and MDIs, which would enable these entities to not just lend, but also grow through acquisition or expansion, thus being able to serve more clients.

Paycheck Protection Program Liquidity Facility (PPPLF)

The Congressionally appropriated SBA Paycheck Protection Program and the Federal Reserve’s related Paycheck Protection Program Liquidity Facility (PPPLF) have provided liquidity totaling more than $180 billion since their inception in 2020. These programs provided funds for 67 nonbanks, many of which were not-for-profit CDFI loan funds, in addition to 38 CDFI banks and MDIs that participated in the PPPLF. In fact, the PPPLF was the most heavily used of the emergency lending facilities established by the Federal Reserve to support the continued flow of credit to households, businesses, and state and local governments during the height of the pandemic.29 The PPPLF provided important support for enabling mission-oriented CDFIs, MDIs, and other small banks to support very small businesses. Among banks that participated in the facility, community banks, including CDFI banks (those with $10 billion or less in assets), have received more than 90 percent of the advances from the PPPLF.30 This example demonstrates that CDFIs and MDIs stepped up to the plate to help ensure pandemic relief capital flowed to the communities and small businesses that needed it most, and that without their efforts, the capital likely would not have reached as deeply into LMI markets.

CDFI Rapid Response Program

As part of the 2021 Consolidated Appropriations Act, the CDFI Fund awarded $1.25 billion to CDFIs in support of communities impacted by the COVID-19 pandemic. The CDFI Fund designed the CDFI Rapid Response Program (CDFI RRP) to quickly deploy capital to Certified CDFIs through a streamlined application and review process.31 The historic pot of award dollars represents a watershed moment. Prior to this appropriation, since its inception in 1994, the CDFI Fund had awarded nearly $3.9 billion to CDFIs through its CDFI Financial Assistance, Bank Enterprise Award, and other programs over 27 years. The $1.25 billion CDFI RRP funding is equivalent to about one-third of that amount, awarded in just one year; 863 qualified CDFIs are currently in the process of deploying these dollars toward financial products and services, loan loss reserves, providing development services, or in the case of depository institutions, capital reserves.32 Further, CDFIs can expend $200,000 or 15 percent of the award value, whichever is greater, toward operations including salaries, fringe benefits, professional services, travel, training and education for staff, as well as equipment and supplies. Recipients will begin providing their first reports about uses of award funds and loan transactions shortly. This information will be of great interest to researchers and policymakers alike once it becomes available to the public, providing a window into how CDFIs met the needs of borrowers and where loans were made, and enable econometric analysis to be conducted to assess the effectiveness of disbursements.

CDFI Minority Lending Program

One program from the 2021 Consolidated Appropriations Act is still under development: the Emergency Support and Minority Lending Program. This program has a $1.75 billion budget intended to expand lending, grant making, or investment activity in LMI minority communities that have significant unmet capital or financial services needs.33 Once available, depository and nondepository CDFIs, including a new category of CDFIs, “minority lending institutions,” can apply for these funds.34 How the CDFI Fund will implement this program remains an open question — and banks should follow developments on the CDFI Fund’s website to determine award eligibility and deadlines once the information is publicly available.

Private Sector and Earned Income

Corporations and private foundations have also substantially increased their investments in CDFIs in light of the pandemic and the racial injustices it highlighted further. Companies such as Netflix, Microsoft, Google, and Nike, as well as philanthropist MacKenzie Scott have all committed to supporting CDFIs and MDIs as a means to promote economic opportunity and racial equity through various investment vehicles and grant funding.35 Meanwhile, S&P-rated nonprofit CDFIs continue to structure bonds with large financial institutions to access long-term, patient capital to address financing challenges that extend beyond a five- or 10-year term, such as affordable housing developments or community health-care centers, which all benefit from 30-year financing terms.36

Challenges CDFIs Still Face

Given the recent increase in the flow of capital to support CDFIs, researching whether the capital flowed to its intended recipients, and identifying the impediments to the flow to end users, will help inform policymakers’ approach to providing access to capital for LMI communities and communities of color, particularly in times of financial distress. It is also important to understand that while the federal pandemic response provided CDFIs with much-needed sources of capital to support their operations and continued lending in economically distressed communities, the pandemic itself also exacerbated the challenges many CDFIs previously faced.

Working within the confines of, and fighting against, institutionalized systemic racism perhaps remains the thorniest challenge for CDFIs. Working with harder-to-reach clients continues to be extremely challenging. Examples of such challenges include: the subjectivity of appraisals that can significantly undervalue properties;37 the need for collateral, which is limited in low-wealth communities of color; requirements for personal guarantees, which can put business owners with limited assets in jeopardy; and a preference for lending to those with the highest credit scores in spite of research and analysis demonstrating that there is bias baked into these scores.38 CDFIs also struggle with how to adjust these requirements so they can ensure repayment, while being flexible in understanding that credit models likely have their own racially motivated biases, and that CDFIs must work harder to reach the communities of color they serve.39

Another challenge is staffing, which in many industries has only become more difficult in the last two years. It takes time to recruit and train culturally competent staff members who understand both CDFI business models and the needs of the clients they serve. Competition for staffing has increased with the growing need for staff to process more requests for financing from clientele. Additionally, the skill sets in CDFIs have evolved, with many CDFIs vying for talented, diverse individuals who can help grow the balance sheets of CDFIs and communicate to the public and investors about the impact CDFIs provide both financially and socially. A recently developed program, the Economic Mobility Corps (EMC), has the potential to address some fluctuating staff issues and build a pipeline of future CDFI practitioners; however, while innovative, with an initial budget to provide 61 full-time AmeriCorps service members to CDFIs over a two-year period, this joint initiative between the CDFI Fund and AmeriCorps will likely only make a small dent in the current dearth of CDFI staffing options.

Back-office management, work that many CDFIs conduct themselves, continues to cause many operational headaches. With increased demand for loans comes an increased need for back-office capacity; however, the ways in which CDFIs model their staffing now, when coffers are full, could have repercussions when demand wanes. Shared service and fee-for-service models can be advantageous; however, many CDFIs prefer to keep many operations in house. Examples include repayment and collection work, which many CDFIs like to perform themselves so they can maintain positive relationships with clients, which in turn can help repayment.40 As balance sheets and the number of transactions grow, and hybrid work models prevail, CDFIs will need to assess the trade-offs between ownership of back-office processes and return on investment. Trade-offs will also be particularly relevant as living in an increasingly digitized world requires budgets and infrastructure to support online access and cybersecurity around the clock.

To this end, partnerships will become increasingly necessary, particularly as competition increases from fintechs and other nonbank financial service providers that can provide fast, digital financing options. Several CDFIs have worked to create partnerships with such organizations, and finding the right strategic partners that are mission-aligned remains of the utmost importance.41 Other partnerships, such as those that CDFIs naturally pursue with employers, utility companies, and other local actors, hold creative potential to address the industry’s latest challenges.

Ebbing loan demand, changes in appropriations, and the appetite of funders will also likely have repercussions for CDFI capitalization. To address potential future funding shortfalls, CDFIs will need to explore capital from other sources such as secondary markets and other private investors. Investments from these sources will require CDFIs to address an issue that has plagued the industry for over a decade, if not longer — the lack of standardized financial data. Determining how to standardize data collection in a nonstandardized industry is no small feat. If successful, CDFIs will be able to provide investors with consistent and transparent information about their operations and loan portfolios, which investors require to justify the investments.42

Finally, the influx of capital from existing federal funding that is currently in play will necessitate adroit compliance, data tracking, and impact evaluation and measurement to meet government requirements. The customized nature of CDFI loan products makes data collection challenging but not impossible. Several CDFIs have mastered this art, and regularly produce reliable, comprehensive data sets. The CDFI Fund itself is continuously working to improve its own data collection systems and instructions, but funding and resources to support the accurate collection of usable, analyzable data at the scale required to conduct meaningful econometric analysis remain elusive.

Conclusion

The Federal Reserve has a longstanding commitment to support the missions of CDFIs and the communities they serve, regardless of the economic cycle in which we may find ourselves. We are at an exciting and important time in the history of the CDFI industry. While CDFIs are not a panacea for our economic challenges, they do play a role in an inclusive recovery from the pandemic and its associated economic turmoil. With the growth that has occurred in the CDFI industry since the mid-1990s, repeated evidence of the ability to respond in times of national economic duress, and the challenges our nation faces in creating an equitable economic recovery from the COVID-19 pandemic, it is no surprise that the tent of partners with the CDFI sector has grown in size. The issue now is to ensure these entities are fully equipped to do this extremely challenging and important work for the long haul and document their success with sound econometric analysis to state with empirical confidence that CDFIs can and do improve economic outcomes for the clients they serve.

ENDNOTES

1 Congress provided $1.25 billion to the CDFI Fund in the 2021 Consolidated Appropriations Act to award grants to CDFIs to deliver assistance to communities impacted by COVID. See CDFI Rapid Response Program (CDFI Fund, June 15, 2021).

2 See Jonathan Shieber, “Vista Partners founder calls for a fintech revolution to help pandemic-hit, minority-owned small businesses” (TechCrunch, May 10, 2020).

3 See Price Fishback, Jonathan Rose, Ken Snowden, and Thomas Storr, “New Evidence on Redlining by Federal Housing Programs in the 1930s” (Federal Reserve Bank of Chicago, January 3, 2022) and Tracing the Legacy of Redlining: A New Method for Tracking the Origins of Housing Segregation (National Community Reinvestment Coalition, February 24, 2022).

4 See the Treasury Department CDFI.

5 See the CDFI Annual Certification and Data Collection Report (ACR): A Snapshot for Fiscal Year 2020 (U.S. Treasury Department, October 2021).

6 See Pub. L 103-325, 108 STAT. 2160 (September 23, 2004). The provisions of the act creating the CDFI Fund appear in subtitle A, “Community Development Banking and Financial Institutions Act of 1994,” and is codified at 12 U.S.C. §4701 et seq.

7 See CDFI Annual Certification and Data Collection Report (ACR): A Snapshot for Fiscal Year 2020.

8 See the Treasury Department FAQs on “Certification, Compliance Monitoring and Evaluation.”

9 CDFIs elect to serve certain target markets, which can be geographical, or focus activities in a nondiscriminatory way on specific low- and moderate-income (LMI) population groups.

10 Such programs include the CDFI Fund’s competitive CDFI and Native CDFI Financial Assistance Programs, and the CDFI Bond Guarantee Program, among others; free training and technical assistance opportunities sponsored by the CDFI Fund; and funding from external parties like foundations, corporations, and philanthropies that focus their work with certified CDFIs. See also “CDFI Certification” (CDFI Fund); Programs | Community Development Financial Institutions Fund; NCUA-CDFI Certification Initiative (National Credit Union Administration).

11 See Michael Swack, Jack Northrup, and Eric Hangen, “CDFI Industry Analysis: Summary Report,” Vol. 24 Community Investments No. 2 (Federal Reserve Bank of San Francisco, 2012); see Community Development Consulting, Inc. for a discussion of CDFI self-sufficiency ratios, where even CDFIs with the highest asset size were not 100 percent self-sufficient. Also note, CDFIs are prohibited from charging excessively high or usury rates, while similar lending businesses without a social mission are not subject to these prohibitions.

12 If you know of a community bank or nonprofit that has inherently been providing socially responsible financial products and services in LMI communities, with an institutional commitment to including those community members within leadership or boards of directors, it might be worth exploring whether applying for CDFI certification could help the entity meet its goals and the needs of the communities it serves.

13 See Annie Donovan, “Outcomes-Based Funding and the Community Finance Ecosystem.”

14 See Jamie R. McCall and Michele M. Hoyman,“Community Development Financial Institution (CDFI) program evaluation: a luxury but not a necessity?”Community Development (October 31, 2021).

15 See Michael Swack, Eric Hangen, and Jack Northrup, “CDFIs Stepping into the Breach: An Impact Evaluation—Summary Report”(August 2014).

16 See Brent Howell, Lisa Mensah, and Dafina Williams, “Lending Where Others Will Not: How CDFIs Build Family and Community Wealth,” Federal Reserve Bank of St. Louis (2021).

17 See “What’s a Capital Stack and How Does It Work?” CRA Today.

18 See Double Jeopardy: COVID-19 and Black Owned Businesses (Federal Reserve Bank of New York, August 2020); Alicia Robb, “Access to Capital Among Young Firms, Minority-owned Firms, Women-owned Firms, and High-tech Firms” (April 2013);. Access to Capital Is Still a Challenge for Minority Business Enterprises |(Minority Business Development Agency, September 2006); Racial Disparities and Housing Policy (Habitat for Humanity, August 2020).

19 See “Access to Access to Capital and Credit in Native Communities and Credit in Native Communities,” (University of Arizona Native Nations Institute).

20 Note to 12 U.S.C. §1463. “‘Socially and economically disadvantaged individuals’ refers to minority communities such as ‘Black American, Asian American, Hispanic American, or Native Americans.”

21 See FDIC: Minority Depository Institutions Program and CDFI Fund’s “List of Certified Community Development Financial Institution (CDFIs) with Contact Information as of December 14, 2021.”

22 See Capital Magnet Fund (CDFI Fund).

23 See Bank Enterprise Award Program (CDFI Fund).

24 See Bank Enterprise Award Program.

25 See Small Dollar Loan Program (CDFI Fund).

26 See Small Dollar Loan Program.

28 Note some CDFIs are also MDIs, and there is overlap in these two numbers. See Emergency Capital Investment Program (Treasury Department); Financial Institutions Approved to Receive ECIP Investments (Treasury Department).

29 See Financial Stability Report: “Borrowing by Businesses and Households” (Federal Reserve Board, May 2021).

30 See Financial Stability Report: “Borrowing by Businesses and Households.”

31 See “U.S. Treasury Awards $1.25 Billion to Support Economic Relief in Communities Affected by COVID-19 (CDFI Fund, June 15, 2021).

32 See CDFI RRP Application Overview Presentation (CDFI Fund, February 21, 2021).

33 See “Treasury to Invest $9 Billion in Community Development Financial Institutions and Minority Depository Institutions Through Emergency Capital Investment Program (ECIP)” (U.S. Department of the Treasury, March 4, 2021).

34 See “Treasury to Invest $9 Billion in Community Development Financial Institutions and Minority Depository Institutions Through Emergency Capital Investment Program.”

35 See Netflix to Invest 2% of Cash Holdings in CDFIs and Other Organizations Serving Black Communities (Opportunity Financial Network, June 30, 2020); Nike, CDFI Leaders Reflect on Company’s Decision to Invest in Opportunity Through Hope Credit Union (Opportunity Financial Network, December 17, 2021); Google Announces New $50 Million Investment in CDFIs and Black Community | Opportunity Finance Network (Opportunity Financial Network, June 18, 2020); FDIC Launches Mission-Driven Bank Fund with Microsoft, Truist to Support CDFIs (Opportunity Financial Network, September 21, 2021); Philanthropist MacKenzie Scott Supports 24 OFN Member CDFIs in Latest Giving (Opportunity Financial Network, December 16, 2020).

36 See Missions Possible: How U.S. CDFIs Meet Financial And Social Missions, and the Rating Implications That Follow (Standards & Poor); LISC Impact Notes Named Social Bond of the Year by Environmental Finance (Local Initiatives Support Corporation, March 31, 2021).

37 In June 2021, the Interagency Task Force of Property Appraisal and Valuation Equity (PAVE) was created to address this issue. Additional information, including a March 2022 report and action plan, is available on PAVE’s website.

38 See Neil Bhutta, Aurel Hizmo, and Daniel Ringo, “How Much Does Racial Bias Affect Mortgage Lending? Evidence from Human and Algorithmic Credit Decisions” (SSRN, July 19, 2021); Ashlyn Aiko Nelson, “Credit scores, race, and residential sorting,” Journal of Policy Analysis and Management (November 30, 2009).

39 See the Letter to Congressional Leaders (April 9, 2020).

40 See “Scaling Lending to Entrepreneurs of Color: Part I Core Operational Challenges” (Aspen Institute).

41 See “TILT Forward Initiative and DreamFund” (Association for Enterprise Opportunity, November 20, 2017).

42 See Sean Campbell and Christopher Shin, “Securitization for Social Innovation: Jump-Starting Commercial Intermediation for the CDFI Industry” (Local Initiatives Support Corporation, January 2021).