Combating Elder Financial Abuse

On October 8, 2009, a jury in New York City convicted Anthony Marshall of defrauding Brooke Astor, his late, elderly mother, of millions of dollars while she suffered from Alzheimer’s disease.1 Because Mrs. Astor was a famous philanthropist, this high-profile criminal case cast a national spotlight on the issue of financial exploitation of the elderly, commonly known as elder financial abuse.

Roughly one in 10 seniors have suffered financial, emotional, physical, or sexual abuse or neglect in the past year, according to one study, with financial abuse occurring the most.2 Many elderly Americans own their own homes and are financially secure, but they may have cognitive impairments, making them prime targets for individuals seeking to exploit their financial assets.3

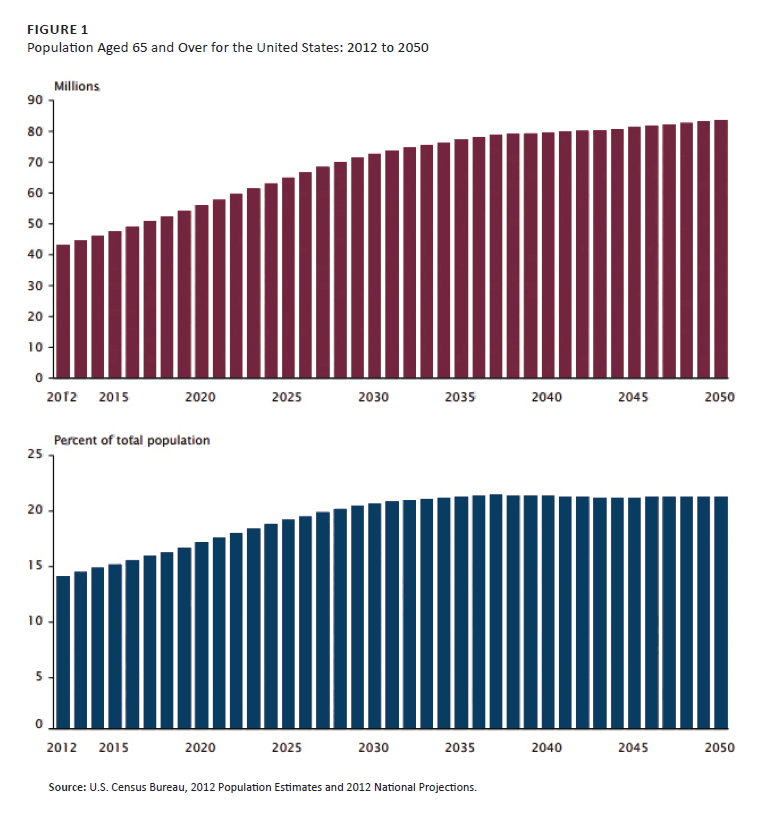

According to a report by the Consumer Financial Protection Bureau (CFPB), the estimated annual losses from elder financial abuse range from $2.9 billion to $36.48 billion.4 Demographic trends suggest this problem will worsen in the future. The U.S. Census Bureau estimates that, by 2050, the population of Americans over the age of 65 will exceed 20 percent of the U.S. population (as shown in Figure 1).

Research indicates that “the ‘typical’ victim of elder financial abuse is between the ages of 70 and 89, white, female, frail, and cognitively impaired.”5 Many news reports feature financial scams by strangers, but the victims usually know the perpetrators. Most often the perpetrators are family members (68%), friends and neighbors (17%), and home healthcare aides (15%).6 Although an estimated 5 million elderly adults experience financial abuse each year, it is believed that many do not report it for a variety of reasons such as embarrassment or fear of retaliation.7

Financial institutions should be aware of the signs of elder financial abuse. Institutions can play a key role in helping to prevent and respond to abuse because they interact directly with customers, have information about customers’ accounts and transactions that may flag potential abuse, and have tools and resources to report suspected abuse. However, some financial institutions are concerned that state and/or federal privacy laws may prohibit them from disclosing their customers’ financial records to authorities and are uncertain of the best way to proceed. To address these concerns, this article reviews federal privacy laws, regulatory guidance, and sound practices that institutions can adopt to help protect their elderly customers from financial abuse.

FEDERAL PRIVACY PROTECTION

Various laws, regulations, and guidance apply to elder financial abuse. The focus here is on federal law and guidance, but financial institutions may also be subject to state and local laws in the jurisdictions in which they do business.8

Sharing Nonpublic Information to Third Parties – The GLBA

What does the law require? Section 502 of the Gramm-Leach-Bliley Act (GLBA) generally prohibits a financial institution from disclosing nonpublic personal information about a consumer to nonaffiliated third parties unless the consumer is notified and has the opportunity to opt out.9 “Nonpublic personal information” (NPPI) generally is any information that is not publicly available and that:

- a consumer provides to a financial institution to obtain a financial product or service from the institution;

- results from a transaction between the consumer and the institution involving a financial product or service; or

- a financial institution otherwise obtains about a consumer in connection with providing a financial product or service.10

What information can financial institutions share related to suspected elder abuse? In 2013, several federal regulatory agencies jointly issued the “Interagency Guidance on Privacy Laws and Reporting Financial Abuse of Older Adults” (guidance) to clarify whether the privacy provisions of the GLBA apply to reporting suspected financial exploitation of older adults.11 The guidance notes that, while the GLBA restricts sharing NPPI, the law contains exceptions, four of which may apply to the reporting of elder financial abuse depending on the particular circumstances of the suspected abuse:

- Protect against or prevent actual or potential fraud, unauthorized transactions, claims, or other liability (Section 502(e)(3)(B))

- Report to law enforcement agencies to the extent specifically permitted or required under other applicable laws, including the Right to Financial Privacy Act (RFPA) (Section 502(e)(5))

- Comply with federal, state, or local laws, rules, and other applicable legal requirements, such as state laws that require financial institutions to report suspected abuse (Section 502(e)(8))

- Respond to a civil, criminal, or regulatory investigation or subpoena or summons by federal, state, or local authorities; or respond to judicial process or government regulatory authorities (Section 502(e)(8))

The guidance also provides the following two examples of permissible disclosure under the fraud exception that are relevant for elder financial abuse:

- Report incidents when an elderly adult’s funds are taken without actual consent

- Report incidents of an older adult’s consent to sign over assets where the intent of the transaction has been misrepresented.

A concluding statement in the guidance is particularly important: “[G]enerally disclosure of nonpublic personal information about consumers to local, state, or federal agencies for the purpose of reporting suspected financial abuse of older adults will fall within one or more of the exceptions.”12

SOUND PRACTICES

Financial institutions can play a critical role in helping to detect and prevent elder abuse. Here are some sound practices for your consideration.

Prevention

The best outcome for financial institutions and their customers is to prevent elder financial abuse from occurring. In March 2016, the CFPB published a comprehensive report titled Recommendations and Report for Financial Institutions on Preventing and Responding to Elder Financial Exploitation that focuses on sound practices to help prevent elder financial abuse. The CFPB’s recommendations include the following:

- Coordinate efforts to better educate older customers and other stakeholders about the problem

- Use technology to flag and to identity warning signs of abuse

- Report suspected abuse to the authorities and develop a relationship with the state adult protective services agency

- Protect account holders; for example, by extending the time period under Regulation E to report unauthorized transactions when a customer has extenuating circumstances, such as hospitalization

The report notes that elders are an attractive target for criminals because of their financial assets and vulnerability and concludes that “financial institutions have a tremendous opportunity to serve older consumers by vigorously protecting them from financial exploitation.” Further details are available in the CFPB’s report.13

Age-Friendly Banking

Age-friendly banking refers to recommendations from the National Community Reinvestment Coalition (NCRC) to improve banking services for older adults.14 Age-friendly banking includes proactive strategies to address the particular needs of elderly customers in their use of banking services. This approach is designed in part to lead to reduced levels of financial abuse and exploitation while leading to increased levels of inclusion and access to the banking system. Principles of age-friendly banking include:

- customizing products for elderly customers and making customer service personnel available with knowledge of the products;

- offering affordable financial management services such as retirement planning;

- ensuring that older adults have access to critical income support programs and electronic benefits;

- incorporating age-friendly design features and training on online banking; and

- establishing a program to identify and report suspected elder financial abuse.15

The Federal Reserve Bank of San Francisco’s Center for Community Development Investments also published a working paper on this issue, “What Can We Do to Help? Adopting Age-Friendly Banking to Improve Financial Well-Being for Older Adults.” The working paper reported that, with the elderly population expected to represent 20 percent of the U.S. population by 2050, financial institutions are instituting age-friendly banking programs. The paper identifies impactful strategies such as maintaining branches in neighborhoods with high percentages of elderly populations and designating “older adult specialist” staff equipped to assist in all issues affecting older adults.16

Training

Training staff, especially tellers, is critical to combating elder financial abuse because they interact directly with elderly customers. The San Francisco Fed working paper found that many elderly consumers are concerned about the safety of online banking, do not own a computer or smartphone, and/or may experience physical limitations that make them less able to rely upon computers for banking purposes.17 It is therefore not surprising that a Federal Deposit Insurance Corporation survey found that more than half of consumers aged 65 or older rely on bank tellers to access bank accounts.18 Additionally, tellers are in a good position to observe suspicious conduct, such as changes in banking patterns and unusual transactions.

Tellers also often develop a relationship with customers and might be able to recognize if a customer is acting in an unusual manner or under duress. The San Francisco Fed’s working paper reported that a large bank partnered with a city agency in Philadelphia to train tellers and customer service staff to identify signs of abuse. More than 3,000 cases were investigated, potential losses of $2.2 million were prevented, and $62.5 million in assets were protected.19 Bank tellers are thus a key resource in the battle against elderly financial abuse.

Identification

Bank staff must be able to identify suspected elder financial abuse before it can be reported. In 2011, the U.S. Department of the Treasury’s Financial Crimes Enforcement Network (FinCEN) issued an alert on elder financial exploitation that encouraged financial institutions to file a Suspicious Activity Report (SAR) when abuse is suspected.20 To assist institutions in identifying possible illicit activity, the advisory listed the following warning signs:

Erratic or unusual banking transactions or changes in banking patterns

- Frequent large withdrawals, including daily maximum currency withdrawals from an ATM

- Sudden nonsufficient fund activity

- Uncharacteristic nonpayment for services, which may indicate a loss of funds or a loss of access to funds

- Debit transactions that are inconsistent for the elderly

- Uncharacteristic attempts to wire large sums of money

- Closing CDs or accounts without regard to penalties

Interactions with older adults or caregivers

- A caregiver or other individual shows excessive interest in the elder’s finances or assets, does not allow the elder to speak for himself or herself, or is reluctant to leave the elder’s side during conversations.

- The elder shows an unusual degree of fear or submissiveness toward a caregiver.

- A representative from a financial institution is unable to speak directly with the elder, despite repeated attempts to contact him or her.

- A new caretaker, relative, or friend suddenly begins conducting financial transactions on behalf of the elder without proper documentation.

- The elder moves away from existing relationships and toward new associations with other friends or strangers.

- The elderly individual’s financial management changes suddenly, such as through a change of power of attorney to a different family member or a new individual.

- The elderly customer lacks knowledge about his or her financial status or shows a sudden reluctance to discuss financial matters.

Periodically incorporating some of the key considerations about elder financial abuse and the warning signs into a financial institution’s staff meetings or training can be an effective reminder. Institutions also can provide sample questions to staff to ask elderly consumers under common red flag scenarios to elicit additional information about potential abuse. Finally, training should include action items to complete when elder fraud is suspected.

REPORTING

Financial institutions should have policies and procedures in place to address the point at which staff should report suspected elder financial abuse, to whom those concerns should be reported, and to designate the person who should be contacted if staff have questions. All states have established an agency responsible for protecting adults, typically called Adult Protective Services. The National Adult Protective Services Association has contact information on its website for all 50 state agencies.21 Finally, as noted earlier, FinCEN issued an advisory in 2011 that encouraged financial institutions to file SARs when abuse is suspected.

CONCLUSION

Financial institutions play a critical role in helping to prevent elder financial abuse. Institutions are encouraged to enhance their policies, procedures, and training to ensure they identify and report suspected elder financial abuse to the appropriate authorities in compliance with applicable laws. Specific issues or questions should be discussed with your primary regulator.

RESOURCES

Links are available to elder financial abuse resources on the Outlook website at consumercomplianceoutlook.org.

Endnotes

1 John Eligon,“Brooke Astor’s Son Guilty in Scheme to Defraud Her,” New York Times, October 8, 2009. On March 26, 2013, the Appellate Division affirmed the verdict. Francis X. Morrissey Jr., an attorney hired by the accused, Anthony Marshall, was also convicted of defrauding Brooke Astor. See courts.state.ny.us/REPORTER/3dseries/2013/2013_02032.htm. ![]()

2 Ron Acierno, Melba Hernandez, Ananda Amstadter, et al., “Prevalence and Correlates of Emotional, Physical, Sexual, and Financial Abuse and Potential Neglect in the United States: The National Elder Mistreatment Study,” American Journal of Public Health, February 2010, 100:2, pp. 292–297, available at ncbi.nlm.nih.gov/pmc/articles/PMC2804623/. ![]()

3 The guidance is available at federalreserve.gov/newsevents/press/bcreg/bcreg20130924a2.pdf. ![]()

![]()

4 Consumer Financial Protection Bureau, Recommendations and Report for Financial Institutions on Preventing and Responding to Elder Financial Exploitation, March 2016, http://files.consumerfinance.gov/f/201603_cfpb_recommendations-and-report-for-financial-institutions-on-preventing-and-responding-to-elder-financial-exploitation.pdf. ![]()

![]()

5 National Center on Elder Abuse, “What We Do, Research, Statistics, Data,” available at https://ncea.acl.gov/whatwedo/research/statistics.html. ![]()

6 National Center on Elder Abuse, “What We Do.”

7 National Center on Elder Abuse, “What We Do.”

8 Some states have permissive reporting regimes for suspected elder abuse, while other states have mandatory reporting. The CFPB has prepared a report on elder financial abuse that discusses the states that require mandatory reporting of suspected elder financial abuse. See Recommendations and Report for Financial Institutions, March 2016, p. 23, fn 40.

9 Codified at 15 U.S.C. §6802

10 12 C.F.R. §1016.3(p)(1)

11 “Interagency Guidance on Privacy Laws and Reporting Financial Abuse of Older Adults,” Board of Governors of the Federal Reserve System, Commodity Futures Trading Commission, CFPB, Federal Deposit Insurance Corporation, Federal Trade Commission, National Credit Union Administration, Office of the Comptroller of the Currency, and Securities and Exchange Commission, September 24, 2013.

12 See “Interagency Guidance,” p. 3.

13 See CFPB, Recommendations and Report for Financial Institutions, March 2016, The CFPB also simultaneously issued a shorter advisory on this issue, http://files.consumerfinance.gov/f/201603_cfpb_advisory-for-financial-institutions-on-preventing-and-responding-to-elder-financial-exploitation.pdf. ![]()

![]()

14 National Community Reinvestment Coalition (NCRC), “Age Friendly Banking: Policies to Protect and Grow the Economic Security of Older Adults,” September 2013, available at www.ncrc.org/fleeced/wp-content/uploads/2013/09/age-friendly-banking-fact-sheet-NEW.pdf. ![]()

![]()

15 NCRC, “Age Friendly Banking.”

16 Maya Abood, Robert Zdenek, and Karen Kali, “What Can We Do to Help? Adopting Age-Friendly Banking to Improve Financial Well-Being for Older Adults,” Federal Reserve Bank of San Francisco Working Paper 2015-01, January 2015, p. 12.

17 Abood et al., p. 8.

18 See fdic.gov/householdsurvey/2013report.pdf. ![]()

![]()

19 Abood et al., p. 11.

20 See fincen.gov/sites/default/files/advisory/fin-2011-a003.pdf. ![]()

![]()