Fintech for the Consumer Market: An Overview

Recent technological innovations are resulting in significant changes to the financial services landscape and have led to the rise of certain nontraditional financial services providers. Commonly known as fintech companies, these providers use advances in technology to develop alternative platforms for financial activities, including consumer and small business lending, securities clearing and settlement, and personal financial planning and investing. Banks, investment advisors, and other traditional financial service providers have also begun adopting new technologies by partnering with fintech firms and/or by developing these new technologies in house.

When the fintech industry began to develop (circa 2007–2013), industry participants and observers emphasized the potential for fintech firms to disrupt traditional banking intermediaries. More recently, however, important fintech and banking leaders have focused on partnerships, collaboration, and other relationships among their firms. Many fintech areas are still in the early phases of development or are undergoing evolution. It is therefore too early to predict fintech’s ultimate impact on the banking system or how traditional financial service providers will adapt. However, it is clear that the combination of advances in technology, new uses of data, and changes in customer preferences and expectations are likely to create lasting structural changes in financial services.

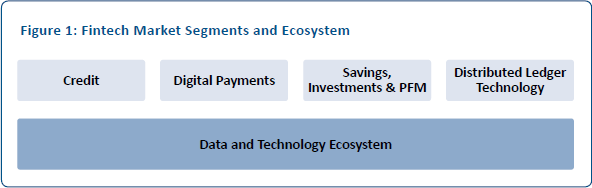

At the Federal Reserve, we are often asked two questions about fintech: (1) What is meant by fintech and (2) what is the Federal Reserve doing to understand the impact of these new technologies? This article attempts to answer both questions by providing an overview of four fintech market segments: credit; digital payments; savings, investments, and personal financial management (PFM); and distributed ledger technology. In addition, this article surveys fintech’s underlying data and technology ecosystem (Figure 1). These segments do not encompass everything that can be considered fintech, but they are among the areas most likely to impact current banking practices and, accordingly, are of particular interest to the Federal Reserve.

CREDIT

Fintech credit providers (alternative lenders) are nonbank lenders that have developed business models based on innovative uses of the Internet, mobile devices, and data analysis technologies. These lenders use technology designed to (1) meet customer expectations for increased speed and convenience (e.g., online applications, documentation transfer, quick decisions on loan approval); (2) provide more clarity and convenience on loan extensions (e.g., pricing, terms, borrower identification); (3) broaden customer sourcing; and (4) automate loan funding. In general, alternative lenders tend to focus on specific segments in the consumer and small business lending space. While alternative lenders are sometimes competitors to banks, the predominant business model is highly reliant on banks to originate and, in many cases, fund their loans. As such, the industry has evolved from direct competition designed to disrupt traditional banking to one of growing partnerships between alternative lenders and banks (Table 1).

Table 1: The Range of Bank Collaboration with Alternative Lenders

|

Funding |

Banks provide funding through loan purchases, credit extensions, and equity investments. |

|

Partnership |

Banks (1) originate loans on behalf of alternative lenders, (2) use technology developed by alternative lenders to originate loans themselves, and (3) direct customers to alternative lenders in exchange for marketing and referral fees. |

|

Incubation |

Banks have provided workspace, seed funding, mentoring, training, and other related support for startup entrepreneurs. |

|

Acquisitions |

Banks have shown some interest in acquiring alternative lenders. |

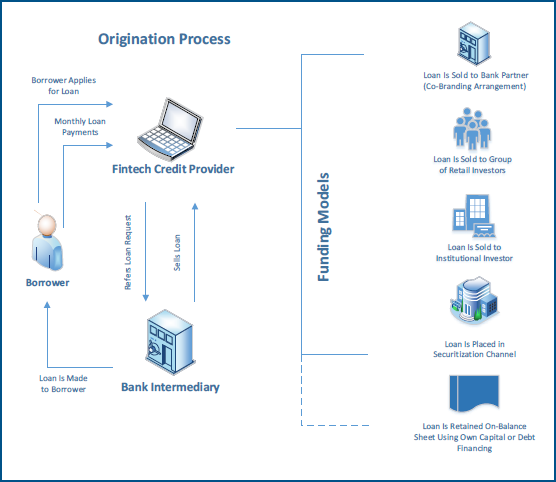

The number and types of alternative lending firms have risen sharply in the past few years, and the business models have evolved. Early firms were referred to as peer-to-peer (P2P) lenders because their business models used technology to directly match prospective borrowers with retail investors to fund specific loans. However, the market has evolved along several dimensions of the business model. The P2P lenders were relabeled as marketplace lenders as firms broadened their funding sources by marketing their loans to institutional investors such as asset managers, hedge fund companies, and banks. Funding also has changed through greater use of loan securitizations and debt financing to fund loans. While most alternative lenders still primarily use a non–balance-sheet or originate-to-sell model, some firms also partly rely on an originate-to-hold/balance-sheet lending model. Figure 2 depicts a typical loan origination process that includes a bank partner that provides the loan and various funding models.

Figure 2: Alternative Lender Loan Origination Process

Many alternative lenders initially focused on unsecured consumer installment debt, often marketed as a means to consolidate and refinance higher-cost revolving credit card debt. Loan types have evolved and now include mortgage, student loan, point of sale financing, and other forms of consumer installment debt, most of which remains unsecured. Small business lending has also become an area of focus for fintech lenders. Firms are able to leverage technology to make loans in smaller amounts or to smaller businesses with revenues that would normally not be profitable for banks. They also can tailor loan and repayment terms based on detailed information about a small business’s daily revenue and finances.

The key distinguishing feature of alternative lenders is their use of the Internet and emerging data-analytic technologies in innovative ways to simplify the customer experience, the loan extension and approval process, and the loan funding process. Online platforms streamline the customer experience when applying for loans, delivering supporting information electronically, signing and reviewing loan documents, and making payments directly from borrowers’ bank accounts. The platforms also are critical for providing information efficiently and seamlessly to investors interested in funding loans.

DIGITAL PAYMENTS

Fintech is changing the way people pay merchants and transfer money, mainly through the use of applications designed for convenience. Such applications are often based on mobile phones with “digital wallets” that store credit card, debit card, and sometimes checking account information, thus eliminating the need for cash or checks. With mobile technology, consumers can use their phones to pay for goods in a checkout line or initiate online payments. In addition, fintech firms have enabled an increasing number of small businesses to accept credit cards as a payment option.

Beyond payments to merchants, firms have developed popular applications that allow people to easily transfer money electronically to any other person. Oftentimes, such transfers are free and can be routed through the use of the recipient’s e-mail address or phone number. In addition to increased convenience when making everyday money transfers such as splitting a lunch bill or paying a sitter, many mobile payment applications offer social networking features that appeal to some consumers.

New payment services also offer greater convenience and ease for business-initiated payments to other businesses and consumers. Through the use of online and mobile payment platforms, businesses can send electronic payments to other businesses for goods and services at a fraction of the cost and time involved with traditional check payments. Other fintech payment services allow businesses to conveniently initiate mass or recurring payments to multiple parties.

Although digital applications present consumers and businesses with easier tools to make payments, fintech firms are still dependent on traditional bank-controlled payment methods (e.g., automated clearing house, credit and debit cards). In this regard, fintech firms need to work closely with banks, either as partners or customers, to transact and settle payments and deposit consumer balances.

SAVINGS, INVESTMENTS, AND PERSONAL FINANCIAL MANAGEMENT

Fintech is also making saving, investing, and PFM more accessible to consumers at all income levels. Fintech efforts in this area tend to focus on (1) automated investment advisory services (commonly known as “robo-advisors”) and (2) financial management tools that collect and analyze consumer habits to simplify saving, investing, and planning. Through innovations in data analysis and other fields, fintech firms in this area can provide investment advice, automatically make investment or savings decisions, and provide resources for budgeting and planning with less need for human interaction and involvement.

Robo-advisors generally employ an online questionnaire to determine a client’s investment objectives and risk tolerance. Using algorithms, the robo-advisor then creates a customized portfolio to fit the client’s need and automatically rebalances the portfolio in response to the performance of the underlying investments and the client’s goals.

Financial management tools include automated savings platforms as well as personal budgeting and financial advice services. These tools analyze consumers’ bank and other financial information. The analysis is then used to assist consumers in meeting their financial goals, in certain cases by offering cost–saving suggestions or even initiating transactions. For example, an automated savings service can analyze and monitor a person’s checking account activity and notify the consumer when it is a good time to transfer funds to a savings account. Making saving and investing easier, with plans available at a modest cost, may benefit consumers.

DISTRIBUTED LEDGER TECHNOLOGY

Distributed ledger technology (DLT), more commonly known as blockchain technology, is a system of decentralized automated record keeping and exchange that creates an immutable record of data that can be automatically and securely updated and stored across a network without the need for trusted central intermediaries.

This technology was popularized in 2009 with the launch of the digital currency and payment system Bitcoin. Since then, it has been used as the foundation to develop other digital currencies and associated payment systems, and many fintech firms have been formed to support these digital currency use cases. After Bitcoin’s introduction, many in the technology and financial services sector recognized the potential of applying DLT to the transfer, clearing, and settlement of more traditional financial market transactions.

A key feature of DLT is that it allows the transfer of an asset without the need for trusted intermediaries, similar to a cash transaction. The technology provides a way to confirm across a network that the sender of an asset is the owner of the asset and has enough of the asset to transfer to the receiver.

DLT may be most transformative when current mechanisms for updating and recording ownership records employ disparate infrastructures and cumbersome processes. Securities trading is one such area in which some fintech and traditional firms are exploring the viability of DLT, because the technology has the potential to reduce clearing and settlement times among broker dealers, exchanges, and custodians. Similarly, other fintech firms and banks are studying DLT to facilitate wholesale, interbank payments with lower costs and faster availability than traditional wire systems.

THE DATA AND TECHNOLOGY ECOSYSTEM

Financial service providers are increasingly relying on a core set of common data and technology systems, including big data, application programming interfaces (APIs), and mobile delivery:

- Big data is an evolving term that describes any voluminous amount of data that has the potential to be mined for information and subjected to new analysis techniques to gain insights into customer behavior.

- APIs are interfaces between different software programs that facilitate their interaction, similar to the way the user interface facilitates interaction between humans and computers. APIs are rules and specifications that software programs follow to communicate with each other.

- Mobile delivery refers to the delivery of financial services via a smartphone or tablet.

Rapid changes have occurred within each of these three areas, fueling their use in the fintech space. For example, advancements in computing power make big data more accessible. In addition, financial services firms are increasingly willing to provide open access to their APIs. Also, the widespread use of smartphones and improved authentication methods have allowed firms to remotely offer an increasing number of services that previously required face-to-face authentication.

The demand for anywhere, anytime mobile financial services is allowing fintech firms to challenge the traditional brick-and-mortar, “9-to-5” banking model. Fintech firms are exploring a wide range of potential uses for big data, APIs, and mobile delivery to better meet customer expectations for on-demand services and to achieve competitive advantages.

FINTECH’S OPPORTUNITIES AND CHALLENGES

Fintech innovations have the potential to benefit both consumers and small businesses. These benefits could include expanding access to financial services, reaching underserved consumers, reducing transaction costs, offering greater convenience and efficiency, and enabling better controls over spending and budgeting.1 Collectively, these innovations may improve the customer experience and permit better alignment of products with the preferences of consumers and small businesses. In addition, these innovations may streamline operations and increase cost efficiencies for banks and fintech firms.

On the other hand, fintech innovations can pose risks for consumers and small businesses. For example, the use of nontraditional data raises questions about the predictiveness of algorithms that have not been tested over a full credit cycle as well as questions regarding fair lending risk. In addition, firms need to control for the privacy and data security risks associated with customer information in an online environment. Ultimately, banks and firms engaged in the fintech space need to ensure that they factor compliance management into their fintech activities to the same extent they factor it into their traditional financial activities, and they need to carefully consider any additional new risks posed as a result of financial innovations.

THE FEDERAL RESERVE’S RESPONSE

The key challenges for regulators are balancing the opportunities and risks as the fintech sector evolves and determining appropriate risk management practices for rapidly evolving technology.2 To this end, the Federal Reserve has formed a multidisciplinary working group that is engaged in a 360-degree analysis of fintech innovation. Working group members have diverse expertise from across the Federal Reserve System, including prudential and consumer supervision, payments, economic research, legal analysis, and community development. Communicating with bankers and fintech firms is a key component of our work as we follow emerging financial technology developments. The working group is an important component of the Federal Reserve’s efforts to foster long-run innovation, including addressing barriers to innovation when appropriate, while ensuring that risks are appropriately controlled and mitigated.

CONCLUSION

Fintech has generated tremendous interest and excitement in the financial services space because of its vast potential to transform how financial services and products are provided to consumers and businesses. But like any other disruptive change, it entails risk. Regulators are trying to find the appropriate balance of facilitating the change, while mitigating and managing the associated risks.

Endnotes

1 For a broader analysis of the potential benefits and risks of fintech, see the discussion with Federal Reserve Governor Lael Brainard.

2 For a more in-depth discussion explaining the interest of bank supervisors in fintech and the careful consideration being given to develop appropriate supervisory policies for the area, see the companion article in this issue titled “Fintech: Balancing the Promise and Risks of Innovation” by Teresa Curran.