Mortgage Disclosure Improvement Act: Corrected Disclosure for an Overstated APR

Imagine for a moment that you have provided a consumer with a Truth in Lending Act (TILA) disclosure statement for a residential mortgage transaction that contains an overstated annual percentage rate (APR). Are you required to provide a corrected disclosure to the consumer and wait three business days before closing the loan, or can you proceed to close the loan because you believe that an overstated APR is always considered accurate under Regulation Z? To redisclose or not to redisclose, that is the question.

During the comment period for the December 2008 proposed implementing regulations for the Mortgage Disclosure Improvement Act (MDIA), the Board of Governors of the Federal Reserve System received comments from many financial institutions and financial services trade associations stating that a three-business-day waiting period before consummation is not warranted if the early TILA disclosure shows an overstated APR because the error benefits the consumer. This is a very common assumption among lenders, which is causing confusion regarding the MDIA's redisclosure requirements.

In the Third Quarter 2010 issue of Outlook, Micah Spector of the Federal Reserve Bank of Philadelphia discussed the timing requirements of the MDIA in an article titled “Mortgage Disclosure Improvement Act (MDIA): Examples and Explanations.”1 This article clarifies the confusion surrounding the MDIA's redisclosure requirement for overstated APRs.

CORRECTED DISCLOSURE REQUIREMENTS

To implement the MDIA's redisclosure requirements, §226.19(a)(2)(ii) of Regulation Z requires lenders to provide a corrected TILA disclosure to the consumer if at the time of loan consummation the disclosed APR is outside the accuracy tolerance in §226.22. Lenders must make corrected disclosures of all changed terms, such as the finance charges and monthly payments, as a result of an APR change and must wait three business days before consummation. Lenders have the option of providing a complete set of new disclosures or redisclosing only the changed terms.

It is important to note that the three-business-day waiting period for corrected TILA disclosures applies only if the changes occurred as a result of an APR error. Otherwise, only the corrected disclosure is required, and lenders do not have to wait three business days before consummation.

Let's take a closer look at §226.22 of Regulation Z, since this section determines whether a lender must provide the corrected TILA disclosure for overstated APRs.

ACCURACY OF APR

Section 226.22(a)(2) states that if a disclosed APR for a regular loan transaction does not exceed the actual APR by more than 0.125 percentage point above or below, then the disclosed APR is considered accurate. For irregular transactions, such as loans with multiple advances, irregular payment periods, or irregular payment amounts, the disclosed APR is considered accurate under §226.22(a)(3) if it does not exceed the actual APR by more than 0.25 percentage point above or below.

Regulation Z also states that for loans secured by real property or a dwelling, a disclosed APR will also be deemed accurate if the error resulted from the disclosed finance charge and the disclosed finance charge is not understated by more than $100 or if it is overstated.2 For example, assume that the actual total finance charge was $1,000 for a transaction secured by real property, but the disclosed APR was calculated based on a finance charge of $925 because the lender failed to include a $75 origination fee in the finance charge, which corresponds to an APR of 12 percent. The actual APR using the $1,000 finance charge would yield 13 percent. Even though the disclosed APR exceeds the legal tolerance by more than 0.125 percentage point (assuming this is not an irregular transaction), the disclosed APR is still considered accurate because the error was caused by the finance charge error, and the finance charge was not understated by more than $100. Therefore, in this example, lenders do not need to provide a corrected TILA disclosure and wait three business days before consummation.

Using the same example above, instead of disclosing a 12 percent APR based on a total finance charge of $925, the lender accidently disclosed a 12.5 percent APR because of an input error. The lender still has an understated finance charge of $75 but the 12.5 percent APR error does not correspond to the finance charge error. The question then is whether the finance charge tolerance still applies in this situation. For this, we will turn to §226.22(a)(5).

ADDITIONAL APR TOLERANCE FOR MORTGAGE LOANS

Section 226.22(a)(5) of Regulation Z provides an additional tolerance for a disclosed APR that is incorrect but is closer to the actual APR than the APR that would be considered accurate because the finance charge was not understated by more than $100 or because it was overstated. Confused? The best way to clarify this section is by illustration.

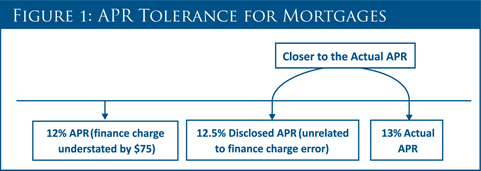

Using the same example as earlier, the lender incorrectly disclosed a 12.5 percent APR due to an input error. The lender also has an understated finance charge of $75, which corresponds to a 12 percent APR. The actual APR is 13 percent based on a total finance charge of $1,000. (See Figure 1 below.)

Figure 1 helps us to understand §226.22(a)(5). Since the disclosed 12.5 percent APR is closer to the actual APR of 13 percent, compared with the 12 percent APR that corresponds to the $75 understated finance charge, the disclosed 12.5 percent APR is considered accurate, even though its computation was not the direct result of the finance charge error. (See Figure 2 below.)

So far, the examples have dealt with understated APRs to help illustrate §226.22(a)(5). Now, let's shift gears toward overstated APRs. The general rule for determining the accuracy of an APR for transactions secured by real property is that if the finance charge is overstated, and as a result, the corresponding APR is overstated, that APR would be considered accurate. Therefore, it is tempting to presume that any overstatement of an APR for transactions secured by real property would never trigger the three-business-day waiting period in addition to redisclosure. However, this presumption is not always correct. Overstatements of APRs can trigger redisclosure along with the three-business-day waiting period, as illustrated in the example below.

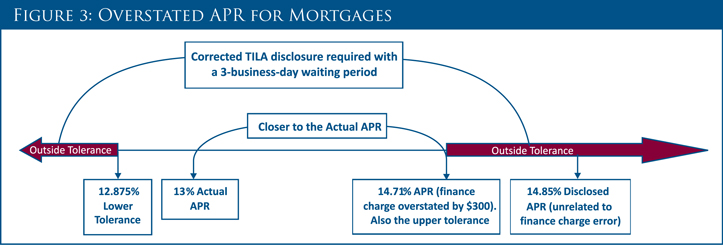

Assume an $8,000 loan secured by real property with an annual interest rate of 13 percent with no prepaid finance charges, and 60 monthly payments of $182.02. However, the lender included a $300 title search fee as a finance charge. The title search fee is not a finance charge. With no other charges except interest, the actual APR in this example would be 13 percent. The APR that corresponds to the $300 overstated finance charge would be 14.71 percent. The lender disclosed a 14.85 percent APR, which is unrelated to the overstated finance charge.

As shown in Figure 3, a disclosed APR that is not the direct result of an overstated finance charge can be subject to redisclosure even if the APR is overstated. Under §226.22(a)(5), if the disclosed APR is overstated beyond the APR that corresponds to the overstated finance charge, 14.71 percent in this example, the disclosed APR is not considered accurate, which triggers the MDIA rules of redisclosure, including an additional three-business-day waiting period.

CONCLUSION

Lenders must be very careful in assuming that overstated APRs do not trigger redisclosure and a three-business-day waiting period. Make sure your system is not automatically set up to generate corrected TILA disclosures only if the disclosed APR is understated. To apply the MDIA rules correctly and avoid violations of Regulation Z, lenders must determine the cause of the overstatement. An overstated APR that corresponds directly with an overstated finance charge is within tolerance and redisclosure is not required. However, not every overstatement of an APR is caused by an overstated finance charge. If there is no finance charge overstatement and the disclosed APR exceeds the 1/8 of a percent tolerance (1/4 of a percent for irregular transactions), or if the disclosed APR exceeds the APR corresponding to an overstated finance charge, redisclosure with a three-business-day waiting period is required. Specific issues and questions should be raised with the consumer compliance contact at your Reserve Bank or with your primary regulator.

- 1 Available at http://www.consumercomplianceoutlook.org/2010/third-quarter/mortgage-disclosure.cfm.

- 2 §226.18(d)(1)